Broadly Accounts are classified as

Account Classification: Broadly Accounts are classified as

Income and Profits

Account Classification: Broadly Accounts are classified as

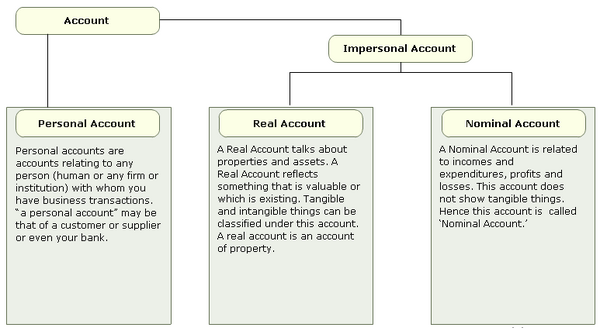

- Personal - Related with the Persons E.g. Mr. Paul’s A/C account at ABC Org

- Nominal - Pertaining to Income and Expenses E.g. Interest, Wages etc.

- Real - Pertaining to things / Properties E.g. Cash , building, Machinery etc .

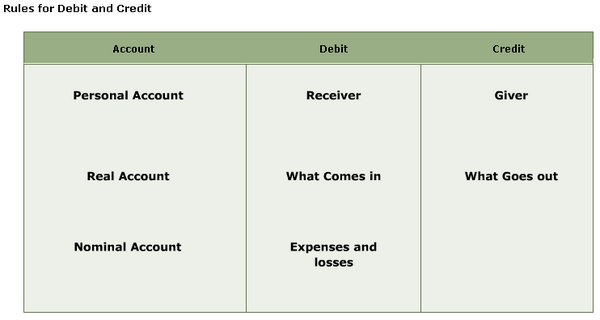

- For Real A/C – Debit that whatever Comes in , Credit whatever goes out.

- For Nominal A/C– Debit expenses, losses and credit incomes and profits.

- For Personal A/C- Debit the Receiver, Credit the Giver.

Income and Profits

Consolidated Statements and Eliminating Entries

Consolidated financial statements are required when there are two or more affiliated companies. When a parent company either directly or indirectly controls a majority interest of a subsidiary, consolidated financial statements must be presented. Consolidated financial statements present the results of operations, statement of cash flows, and financial position of the combined entity. Separate accounting records are kept for each separate company, but not for the consolidated entity. To determine the consolidated amounts, the amounts for the individual affiliated companies are added together. Elimination entries are made to remove the effects of inter-company transactions.

When one company acquires another company, a consolidated balance sheet needs to be prepared. The first step is to eliminate the effects of any inter-company transactions. There are three basic types of inter-company eliminations. The first type is the elimination of inter-company stock ownership. This entry eliminates both the asset and the stockholders’ equity accounts for the parent company’s ownership of the subsidiary.

When one company acquires another company, a consolidated balance sheet needs to be prepared. The first step is to eliminate the effects of any inter-company transactions. There are three basic types of inter-company eliminations. The first type is the elimination of inter-company stock ownership. This entry eliminates both the asset and the stockholders’ equity accounts for the parent company’s ownership of the subsidiary.

The second type of inter-company elimination is the elimination of inter-company debt. When the parent company makes a loan to a subsidiary, the parent company would have a note receivable and the subsidiary a note payable. When the two companies are consolidated, or combined, the loan is just a transfer of cash, so both the note receivable and note payable are eliminated.

The third type of inter-company elimination is the elimination of inter-company revenue and expenses. These inter-company revenues and expenses are eliminated since they are really just transfers of assets from one affiliated company to another and have no effect on consolidated net assets. Some examples of inter-company revenues and expenses are sales to affiliated companies, cost of goods sold as a result of sales to affiliated companies, interest expense or revenue on loans to or from affiliated companies, and rent or other revenue received or paid for services either rendered to or received from affiliated companies.

An important item to understand in regard to consolidated financial statements is the concept of minority interest. A minority interest exists when a parent company owns a majority interest in a subsidiary, but not 100% of the outstanding shares. In this case, the minority interest would be shown on the balance sheet as a type of ownership equity. The minority interest is the ownership interest in the subsidiary that is held by stockholders other than the parent company. Since there are minority stockholders, just the amount of the stockholders’ equity that is owned by the parent company is eliminated.

One of the GAAP guidelines related to consolidated financial statements states that the retained earnings of a subsidiary company that were created before the date of its acquisition can’t be included in the consolidated retained earnings of the parent company and its subsidiaries. In addition, any dividends declared from those retained earnings can’t be included in the parent company’s net income. GAAP also states that comparative financial statements are preferred for annual reports.

Eliminating Entries

The purpose of eliminating entries is to reflect the amounts that would appear if all the legally separate companies were actually a single company.

Eliminating Entries

The purpose of eliminating entries is to reflect the amounts that would appear if all the legally separate companies were actually a single company.

Elimination entries appear only in the consolidating workpapers and do not affect the books of the separate companies.

For the most part, companies that are to be consolidated record their transactions during the period without regard to the consolidated entity.

- Transactions with related parties tend to be recorded in the same manner as those with unrelated parties.

- Elimination entries are used to increase or decrease (in the workpaper) the combined totals for individual accounts so that only transactions with external parties are reflected in the consolidated amounts.

- Some eliminating entries are required at the end of one period but not at the end of subsequent periods.

- For example, a loan from a parent to a subsidiary in December 20x1, repaid in February 20x2, requires an entry to

- eliminate the intercompany receivable and payable on December 31, 20x1, but not at the end of 20x2.

- Some other elimination entries need to be placed in the consolidated workpapers each time consolidated statements are prepared for a period of years.

- For example, if a parent company sells land to a subsidiary for $5,000 above the cost to the parent, a workpaper entry is needed to reduce the land amount by $5,000 each time a consolidated balance sheet is prepared, for as long as the land is held by an affiliate.

- It is important to remember that elimination entries, because they are not made on the books of any company, do not carry over from period to period

--------------------------------------------------------------------------------------------------------------------------------------------------

Basics of Accoutning

Financial statements (or financial reports) are formal records of a business' financial activities. it provide an overview of a business' financial condition in both short and long term. There are four basic financial statements

1. Balance sheet: also referred to as statement of financial position or condition, reports on a company's assets, liabilities, and net equity as of a given point in time.The balance sheet is the snapshot of the assets and liabilities the company has acquired since the first day of business.

See example of a balance sheet @

http://investor.google.com/releases/2009Q2_google_earnings.html

2. Income statement: also referred to as Profit and Loss statement (or a "P&L"), reports on a company's income, expenses, and profits over a period of time. in simple words its a summation of the income and expenses from the first day of this accounting period (probably from the beginning of this fiscal year).

3. Statement of cash flows: reports on a company's cash flow activities, particularly its operating, investing and financing activities.

4. Statement of retained earnings: explains the changes in a company's retained earnings over the reporting period.

In British English, including United Kingdom company law, financial statements are often referred to as accounts, although the term financial statements is also used, particularly by accountants.

In order understand the financial statements one should understand the below terms

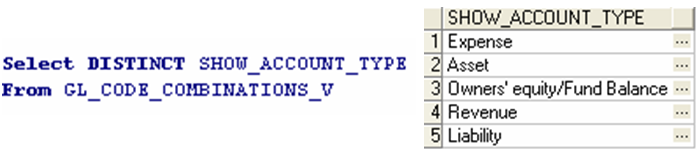

Standrad Oracel has following 5 accoutning types

1. Balance sheet: also referred to as statement of financial position or condition, reports on a company's assets, liabilities, and net equity as of a given point in time.The balance sheet is the snapshot of the assets and liabilities the company has acquired since the first day of business.

See example of a balance sheet @

http://investor.google.com/releases/2009Q2_google_earnings.html

2. Income statement: also referred to as Profit and Loss statement (or a "P&L"), reports on a company's income, expenses, and profits over a period of time. in simple words its a summation of the income and expenses from the first day of this accounting period (probably from the beginning of this fiscal year).

3. Statement of cash flows: reports on a company's cash flow activities, particularly its operating, investing and financing activities.

4. Statement of retained earnings: explains the changes in a company's retained earnings over the reporting period.

In British English, including United Kingdom company law, financial statements are often referred to as accounts, although the term financial statements is also used, particularly by accountants.

In order understand the financial statements one should understand the below terms

Standrad Oracel has following 5 accoutning types

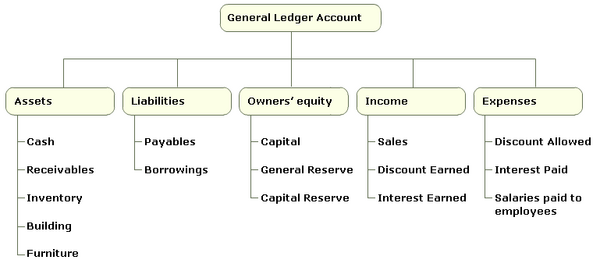

Debit/Credit are the most fundamental concepts in accounting, representing the two records that one party in a transaction makes on its records, transferring a money balance from one account to another, one representing a reduction of liability or increase in asset, and the other representing a balancing increase in liability or reduction of asset.Asset/Liability, Expense/Income are the four baisc type of accounts.

Debit/Credit:

Debit/Credit:

Debits and credits are a system of notation used in accounting to keep track of money movements (transactions) into and out of an account: money paid into an account is a debit, money taken out of an account is a credit. Traditionally, an account's transactions are recorded in two columns of numbers: debits in the left hand column, credits in the right. Keeping the debits and credits in separate columns allows each to be added up independently so that the total debits and credits can be calculated; the smaller of the two totals is then subtracted from the larger to get the account balance. If an account has a debit balance then it owes money (to someone) because more money has been paid into it than has been drawn out, if it has a credit balance then it is owed money.I find the best way to understand debits and credits is to identify two components of each transaction:

1. what did you get?

2. where did it come from?

1. what did you get?

2. where did it come from?

The debit is what you got and The credit is the source of the item you received.

For instance, let's imagine that you purchase a computer with your credit card. Since the computer is what you received it's going to result in a debit to the asset account for your computer. The credit will be applied to the credit card liability account for the same amount.What is often confusing is that the notion of debit and credit will depend on the perspective of the person preparing the accounts, even though they may be essentially the same account. Take your bank account for example. In your accounts when you pay money into your bank account it is recorded as a debit, your bank account is in debt to you - the bank owes you money. The bank's perspective is different however, their job is to keep track of where all the money in their 'vault' has come from and where it goes. To do this, they create an account for each customer so when you pay money into the bank, from their perspective, it has come out of your account (a credit) into their vault: your account is in credit - your account is owed money. When you receive a statement from your bank, it will give the state of your account from the bank's point of view, which is why people are used to the term 'your account is in credit' to mean that they have money in that account, when technically it means the opposite.

The accounts are collectively referred to as the ledger. A journal is a place where entries (debits and credits) are written before they are written in the ledger. Modern computer systems generally have you make entries directly to the ledger and then produce printouts that are designed to look as if they were journals, which they may not be in reality.

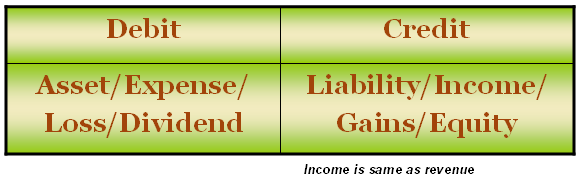

Debits and credits are neither positive nor negative values. The balance on an account is either a debit or a credit, not a positive or a negative value. Dividend, Expense, Asset and Losses (abbreviated as "D-E-A-L") accounts increase in value when debited and decrease when credited, whereas Gains, Income, Revenues, Liability and Stockholder's (Owner's) equity (abbreviated as "G-I-R-L-S") accounts decrease in value when debited and increase when credited.

What are Debtors/Creditors ?

Debtors are people or other firms who owe money to the firm. This will usually happen where the firm has sold goods with a period of credit. The firm sells the good or service but allows the purchaser a period of credit to pay - usually a month. During this month the purchaser owes the firm the money and is therefore a debtor.

If the firm has debts these are considered an asset, because when the debtors pay the firm will have converted the debt into cash in the bank. Because most debts are relatively short-term they are considered current assets. The other current assets are stocks and cash.

The amount of debtors a firm has depends on the line of business they are in. If most of their business is with trade customers where they have to offer credit then the level of debtors may be high. For many retail businesses, however, the level of debtors will tend to be relatively low as most of their sales are cash sales.

Creditors are liabilities. They are the businesses and people to whom the business owes money. Debtors are the businesses and people who owe the business money, and so are assets of the company.

For instance, let's imagine that you purchase a computer with your credit card. Since the computer is what you received it's going to result in a debit to the asset account for your computer. The credit will be applied to the credit card liability account for the same amount.What is often confusing is that the notion of debit and credit will depend on the perspective of the person preparing the accounts, even though they may be essentially the same account. Take your bank account for example. In your accounts when you pay money into your bank account it is recorded as a debit, your bank account is in debt to you - the bank owes you money. The bank's perspective is different however, their job is to keep track of where all the money in their 'vault' has come from and where it goes. To do this, they create an account for each customer so when you pay money into the bank, from their perspective, it has come out of your account (a credit) into their vault: your account is in credit - your account is owed money. When you receive a statement from your bank, it will give the state of your account from the bank's point of view, which is why people are used to the term 'your account is in credit' to mean that they have money in that account, when technically it means the opposite.

The accounts are collectively referred to as the ledger. A journal is a place where entries (debits and credits) are written before they are written in the ledger. Modern computer systems generally have you make entries directly to the ledger and then produce printouts that are designed to look as if they were journals, which they may not be in reality.

Debits and credits are neither positive nor negative values. The balance on an account is either a debit or a credit, not a positive or a negative value. Dividend, Expense, Asset and Losses (abbreviated as "D-E-A-L") accounts increase in value when debited and decrease when credited, whereas Gains, Income, Revenues, Liability and Stockholder's (Owner's) equity (abbreviated as "G-I-R-L-S") accounts decrease in value when debited and increase when credited.

What are Debtors/Creditors ?

Debtors are people or other firms who owe money to the firm. This will usually happen where the firm has sold goods with a period of credit. The firm sells the good or service but allows the purchaser a period of credit to pay - usually a month. During this month the purchaser owes the firm the money and is therefore a debtor.

If the firm has debts these are considered an asset, because when the debtors pay the firm will have converted the debt into cash in the bank. Because most debts are relatively short-term they are considered current assets. The other current assets are stocks and cash.

The amount of debtors a firm has depends on the line of business they are in. If most of their business is with trade customers where they have to offer credit then the level of debtors may be high. For many retail businesses, however, the level of debtors will tend to be relatively low as most of their sales are cash sales.

Creditors are liabilities. They are the businesses and people to whom the business owes money. Debtors are the businesses and people who owe the business money, and so are assets of the company.

Regards

ReplyDeleteSridevi Koduru (Senior Oracle Apps Trainer Oracleappstechnical.com)

Please Contact for One to One Online Training on Oracle Apps Technical, Financials, SCM, SQL, PL/SQL, D2K at sridevikoduru@oracleappstechnical.com | +91 - 9581017828.